by Jon Anderson

Candy's Dirt

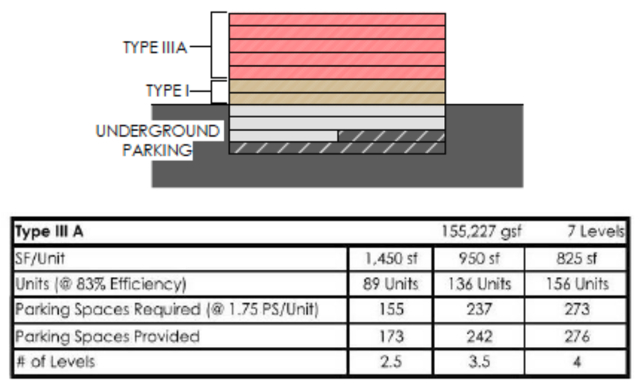

Example of seven-story building construction and density options

A.G. Spanos has released a second, more thorough economic analysis of the feasibility of redeveloping Pink Wall parcels within the confines of the Preston Road and Northwest Highway Area Plan (PRNHAP). Spanos has a contingent contract to redevelop the Diplomat condos within PD-15 and has financed both viability studies. While Spanos has obvious motives, any economic data supplied is certainly more than the economic nothingness contained within the $350,000 PRNHAP study. How the city adopted that Santa’s lap of a plan, containing no financial underpinnings, still astounds.

You’ll recall that in October 2017, my rough calculations exposed the then 10-month old PRNHAP as economically bogus. That was followed up in January 2018 by Spanos’ first report developed by architects Looney Ricks Kiss that backed-up my findings. Namely that the recommendations contained within the PRNHAP study’s “Zone 4” are not viable to build. This latest study offers more detailed and dire details for the PD-15 area (download here).

To be clear, “not economically viable” means that a condo unit would sell for more money as a condo than as developable land. To sell under those conditions would equate to owners taking a loss on their home. In many cases it’s good when land is worth some fraction of a structure. It helps with neighborhood stabilization, curbing gentrification, etc.

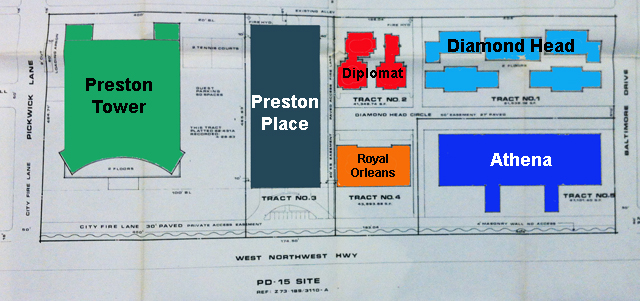

PD-15 area

However, neighborhood revitalization is hampered when the combination of land costs and development rights are less than the value of existing development. I catch flak for “secretly” wanting to bulldoze the Pink Wall and put up acres of junky apartments. I don’t. But I do realize that some Pink Wall buildings have undercharged their HOA dues, resulting in years or decades of deferred maintenance. A cursory glance tells me that Imperial House is the only building to have swapped their original inefficient windows, let alone the number of hidden plumbing, foundation and electrical issues that continue to mount. Residents of more than one Pink Wall complex have told me that while they look good on the outside, they’re rotting on the inside.

The Latest Study

Produced by internationally known real estate consulting firm HR&A, the 18-page report isn’t for the feint hearted looking for a quick read. The firm’s business ranges from High Line Park and a five-year advisor on energy efficiency in New York to analyzing Dallas’ underinvestment in its park system. Author Joseph Cahoon has extensive work experience in multi-family residential development and is an adjunct professor and Director for the Folsom Institute for Real Estate at SMU’s Cox School of Business. In a word, qualified.

For the uninitiated, the document is dense, probably requiring more than one read-through (I did). There’s jargon that won’t be immediately comprehended, so before we discuss, here’re the two biggies:

Residual Land Value: The cost of land. We typically think of land prices from a seller’s point of view. But from a developer’s viewpoint, land value is backed into by deconstructing the total cost and ultimate selling value of a building (rent, cap rate, profit margins). Therefore, residual land value is how much a developer can pay for land minus the costs of a project and expected cap rate (below).

Capitalization or “Cap” Rate: The initial yield or profit margin expected from the project (total generated rent minus construction and long- and short-term operating costs).

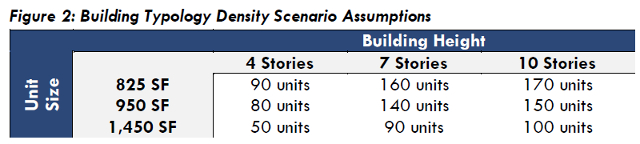

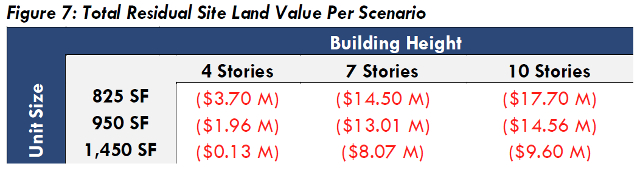

With that in mind, the study builds out nine scenarios (three heights, three average unit sizes). The four-story examples adhere to the PRNHAP study’s height and underground parking limitations. The seven- and 10-story scenarios are three-story steps in height, taller than the PRNHAP study allows, but do include completely underground parking.

Ignoring PD-15’s density limitations, the assumed number of units are what could be built on an acre of land with reasonable setbacks. Extrapolating these to the larger Preston Place and Diamond Head lots or Royal Orleans’ smaller buildable lot would adjust unit counts accordingly (but not linearly as larger and smaller lots offer different economies of scale).

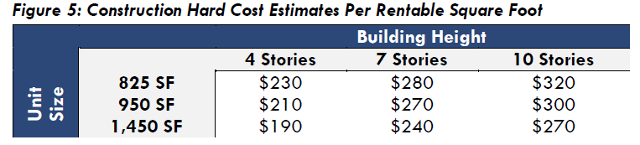

Next is the estimation of construction costs per square foot based on unit counts, size and underground parking. Construction costs may appear high but they include all underground parking (expensive) and also factor in the tighter one-acre example lot. Smaller lots are less efficient to build on. Construction costs relating to the two-acre Preston Place costs would be lower, all things being equal.

Filtered into the numbers is the type of construction. Four-story construction would be wood “stick” construction above ground sitting on 1.5 to 2.5 levels of underground concrete parking (depending on unit size/count – fewer/larger units require less parking). Of the three this is obviously the cheapest to build and can be seen at the Laurel on Northwest Highway and Preston Road.

With seven stories, hybrid building techniques come into play. From the bottom, there would be 2.5 to four levels of underground parking. Concrete would continue for an additional two stories of apartments above ground before five stories of stick construction for the bulk of units. These are sometimes called “five over two” buildings

At 10 stories, there would be 2.5 to 4.5 levels of underground parking with a full 10 stories of concrete construction. You may be wondering why the uplift to all-concrete is less than the difference between the four and seven story examples if concrete is supposed to be so much more expensive. Two points: There isn’t a lot of difference in the number of total units between seven to 10 stories due to lot coverage differences (a 10-story building covers less lot). Essentially adding 10 units (and three stories) to the seven story model raises overall costs nearly 15 percent. Because of the small number of units added, there’s not much more underground parking required either. Lot coverage could be increased were the pool placed on the roof (which would add height and/or cannibalize a whole floor).

The 10-story example is what I call the “no man’s land” of building. The gains over a hybrid building aren’t enough to justify going all concrete (unless you go higher).

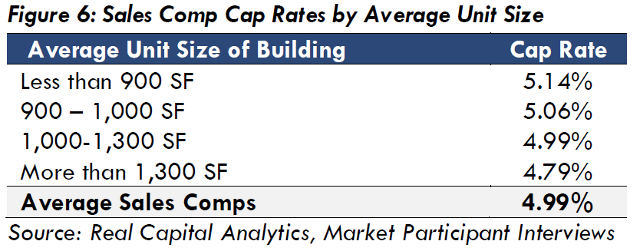

Studying the Dallas area, the report sets a 5 percent return (cap rate) as the average based on comparable buildings. By comparison, the interest rate on a no-risk 10-year Treasury note is currently around 2.85 percent. A cap rate less than the Treasury rate wouldn’t make sense for the risk involved. Risk comes from a variety of factors including future property taxes and chargeable rents.

There’s a lot of red in this table. Essentially, based on the PRNHAP study, none of the four story scenarios are cost effective to build in the current market. The higher buildings even less so.

The report concludes with the understanding that the PRNHAP study is economically unworkable if the goal is to revitalize the neighborhood as it claims. Even at its best, can you imagine the Preston Place owners paying a developer $260,000 (double lot) to build a four-story building with average units of 1,450 square feet?

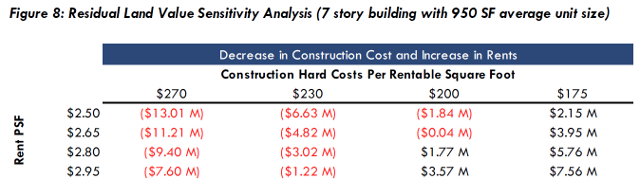

The report states that in order for the math to work, there has to be give in the PRNHAP study and/or rents will have to rise well above expected rates in a market where the high-end is cooling. There’s little anyone can do about rents, but construction costs are another ball game.

Underground Parking

One of the big levers is the preference for completely underground parking. The cost differential between above- and below- ground parking is roughly two- or three-to-one. Were some of the parking allowed above ground, the economics shift for the taller buildings. But the four-story would need to trade residential space for parking, reducing unit counts (and profitability) and therefore it never reaches economic viability. Played out …

Take the mid-sized example of 950 square foot units — 80 units in total and two full underground parking levels. Bringing those two floors above ground could cut the unit count in half to 40. But 40 units wouldn’t need two floors of parking, so call it a single floor of above ground parking with three levels of 60 apartments. While you’d save the excavation costs of the parking, you’d still incur the concrete costs of the above ground garage (can’t park cars in a wood parking lot). Net-net, the reduced unit counts would reduce the profitability so you’d still be in the hole (and so no one would build it).

Looking at the seven- and 10-story examples and it appears that those projects are even more unprofitable. But there’s opportunity in their height and resulting unit counts to enable some above ground parking (wrapped inside the building and invisible outside) to make the numbers work.

Combining an ability to increase to seven stories with a mixture of above and underground parking gets you so far. Building a better quality building that generates slightly more rent is the intersection where developer, seller, and neighborhood meet.

With the ongoing trade war impacting raw material pricing and the ongoing shortage of construction workers that federal immigration policy is exacerbating, construction margins are more on a razor than a year ago when labor shortages alone had raised prices.

A little on the nose?

Some of you may be thinking that this research plays suspiciously into Spanos’ hands because their proposal is for just such a seven-story building at Diplomat. But here’s the thing, this isn’t Spanos’ first turn on the dance floor. Surely they ran their own numbers before deciding to proceed. After all, they spent a year measuring, drilling core samples, negotiating and crunching numbers before writing their contract for Diplomat. Like Goldilocks, the four-story was too little, and the 10-story wasn’t worth the aggravation for little upside, but the seven-story was just right.

And sure, there are ways to push and pull the metrics that the PD-15 authorized hearing can explore to further fine tune things for the neighborhood. Just remember that higher margins enable a developer to give back more to the neighborhood. Higher density also allows for the costs of givebacks to be spread out. Balance is key.

At any rate, this new report gives committee members (and the neighborhood at large) some idea of the financial aspects in redevelopment.

Finally, to those praying at the altar of the Preston Road and Northwest Highway Area Plan, where are your numbers? We know none of the $350,000 spent was for economic modeling to back up its desires, but how about now?

View article online